If the organization is using some kind of accounting software, the bookkeeper or accountant just needs to pass the journal entries (including adjusting entries). The software automatically adjusts and updates the relevant ledger accounts and generates financial statements for the use of various stakeholders. Both the debit and credit columns are totaled at the bottom and must be equal in order to agree with the accounting equation. If the debits and credits don’t agree, there must have been an error posting the adjusting journal entries. In a manual accounting system, an unadjusted trial balance might be prepared by a bookkeeper to be certain that the general ledger has debit amounts equal to the credit amounts. After that is the case, the unadjusted trial balance is used by an accountant to indicate the necessary adjusting entries and the resulting adjusted balances.

Best Wholesale Distribution Software for Small Businesses

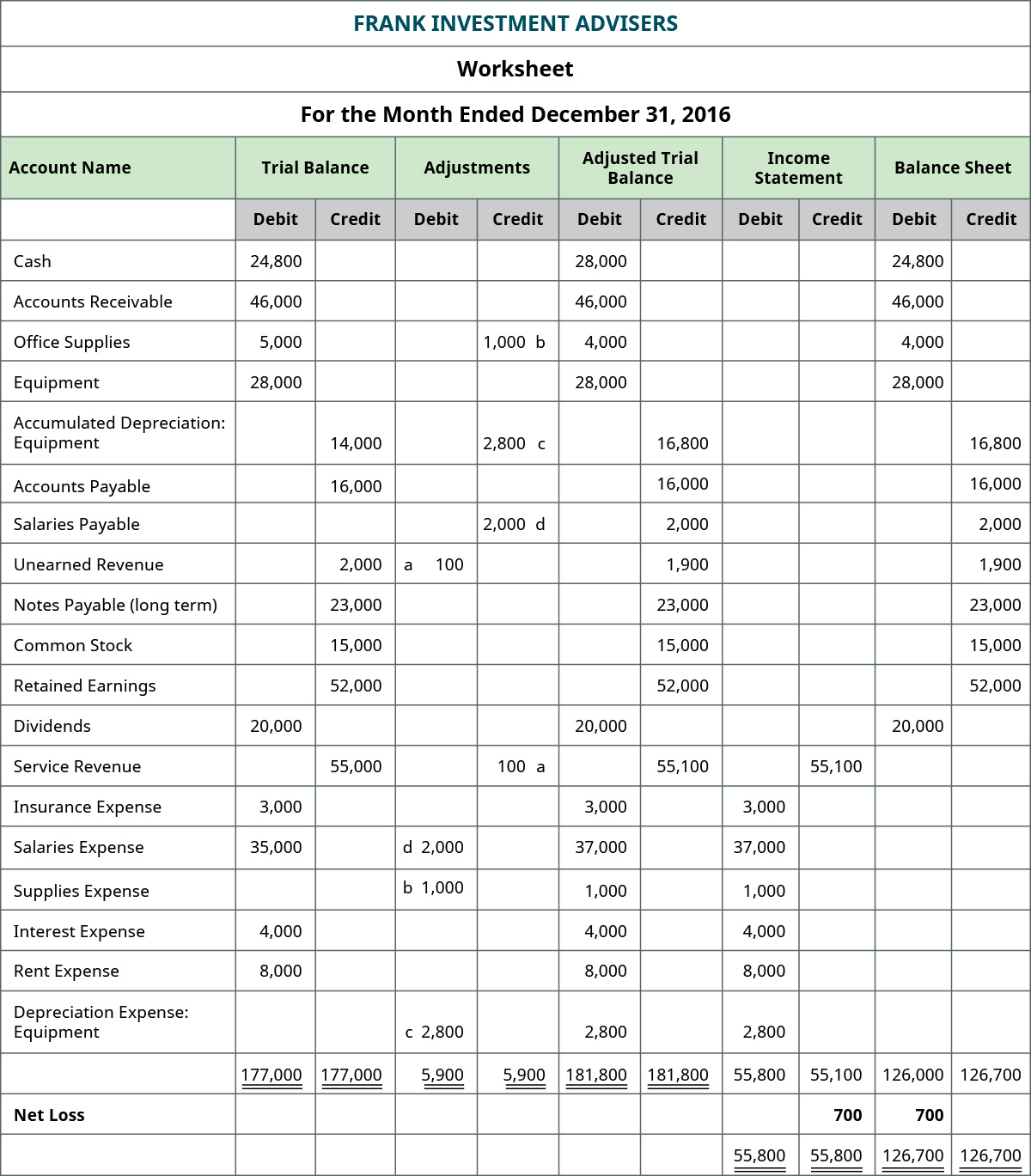

The next step is to review these accounts to determine any that need updating to reflect current financial realities. You could post accounts to the adjusted trial balance using the same method used in creating the unadjusted trial balance. The account balances are taken from the T-accounts or ledger accounts and listed on the trial balance. Essentially, you are just repeating this process again except now the ledger accounts include the year-end adjusting entries. The adjusted trial balance is the key point to ensure all debitsand credits are in the general ledger accounts balance beforeinformation is transferred to financial statements. Budgeting foremployee salaries, revenue expectations, sales prices, expensereductions, and long-term growth strategies are all impacted bywhat is provided on the financial statements.

When to use trial balances

Begin by listing all accounts along with their adjusted balances in a trial balance format. Next, make sure that the total debits equal the total credits, thereby confirming that the adjusted trial balance is in balance. Preparing an adjusted trial balance begins with gathering all necessary financial information. This involves ensuring that all journal entries have been accurately posted to the general ledger. Having a complete and updated ledger is fundamental as it serves as the primary source for identifying which accounts require adjustments.

Adjusted Trial Balance vs Unadjusted Trial Balance

Three columns are used to display the account names, debits, and credits with the debit balances listed in the left column and the credit balances are listed on the right. A balanced trial balance hints at no apparent accounting error, whereas discrepancies imply an error somewhere in the account balances. A trial balance is an accounting report that lists the ending balances of general ledger accounts to ensure the debit and credit balances are equal. As with the unadjusted trial balance, transferring informationfrom T-accounts to the adjusted trial balance requiresconsideration of the final balance in each account. If the finalbalance in the ledger account (T-account) is a debit balance, youwill record the total in the left column of the trial balance. Ifthe final balance in the ledger account (T-account) is a creditbalance, you will record the total in the right column.

- This involves debiting an asset account, such as Accounts Receivable, and crediting a revenue account.

- This adjustment is necessary to account for the wear and tear, obsolescence, or reduction in value of an asset over time.

- Business owners and accounting teams rely on the trial balance to create reliable financial statements.

- If the finalbalance in the ledger account (T-account) is a debit balance, youwill record the total in the left column of the trial balance.

- The format of an adjusted trial balance is same as that of unadjusted trial balance.

- Depreciation is the systematic allocation of the cost of a tangible fixed asset over its useful life.

Thistrial balance is an important step in the accounting processbecause it helps identify any computational errors throughout thefirst five steps in the cycle. This step updates the individual account balances to reflect the adjustments. Ensure that the ledger balances are accurate and match the adjustments made.

Its purpose is to ensure that the total amount of Debit Balance in the general ledger is equal to the total amount of Credit Balance in the general ledger. Adjusted trial balance records the account balances of an organization after adjusting the transaction to various expenses, including the depreciation amount, accrued expenses, payroll expenses, etc. This trial balance type allows businesses have a summarized view of all the account balances post-adjustment to respective expenditures. The adjusting entries are shown in a separate column, but in aggregate for each account; thus, it may be difficult to discern which specific journal entries impact each account. A trial balance is an accounting report you put together at the end of an accounting period to ensure the general accounting ledger is correct and the total debits match the total credits. An adjusted trial balance is formatted exactly like an unadjusted trial balance.

The unadjusted trial balance is the initial report you use to check for errors, and the adjusted trial balance includes adjustments for errors. While an unadjusted trial balance may uncover mathematical errors, the following types help in eliminating accounting errors and ensuring accurate financial statements. Check each account balance to ensure you have made all adjustments correctly and that the totals are accurate. i filed using turbotax live deluxe to see if tax This step is crucial for ensuring that the financial statements prepared from this trial balance will be accurate. An adjusted trial balance is a listing of the ending balances in all accounts after adjusting entries have been prepared. Once all ledger accounts and their balances are recorded, thedebit and credit columns on the adjusted trial balance are totaledto see if the figures in each column match.

It’s also important to consider depreciation and amortization, as these non-cash expenses must be accounted for to accurately reflect asset values. Accurate financial reporting is essential for any business, and an adjusted trial balance ensures this accuracy. By verifying that all accounts are balanced after adjustments, businesses can confidently prepare their financial statements. Bookkeepers, accountants, and small business owners use trial balances to check their accounting for errors.